| 🔍 > Lean Terms Directory |

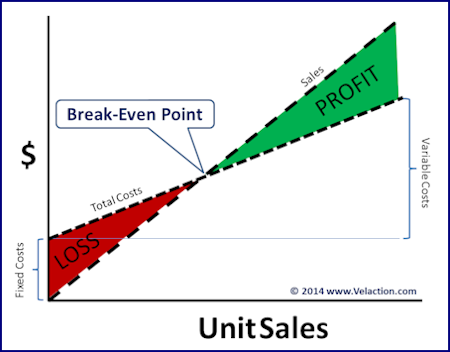

Break-Even Point

The break-even point is the point (number of units sold) where the company can “break-even” and start earning profit.

When a product or service is sold to a customer, the company incurs both fixed and variable costs. Fixed costs are the same regardless of the number of units sold. Variable costs are dependent on the production rate. Rent for production space, for example, is fixed. It has to be paid whether you build 0 or a million widgets in it. The costs for the components in the widgets, however, are incurred at a direct ratio to the number of units produced.

What that means is that in each time period, before you start earning profit, you have to pay off the fixed costs. The break-even point occurs when selling that last unit has paid all the fixed bills. After that point, the difference between the variable costs and the selling price is all profit.

Lean efforts affect the break-even point in one of three ways.

- It makes fixed assets more efficient, so you can reduce your fixed costs. For example, if you reduce the floor space required for a production line, you save on your fixed expenses.

- You can reduce your variable expenses. Lower scrap, for example, or higher quality both bring down unit costs. Higher productivity also reduces variable costs. This flattens the cost line and shifts the break-even point to the left.

- Continuous improvement increases the selling price. As greater value is added, whether through shorter lead times or a willingness of customers to pay for higher quality, the unit price can go up.

Variable vs. Fixed Costs

Note that with enough change in demand, all costs will rise. You can outgrow a factory or might need to add to the support staff. You also don’t typically hire people on a daily basis to match staffing to demand. Consider costs in a narrow band close to current demand—perhaps plus or minus 20%. Also think of what you could do if the demand shifted. You could not pay only half of your rent. You could not decide not to heat the facility. You could, however, cut back on overtime, reduce the number of temp workers you are using, or order fewer components.

0 Comments